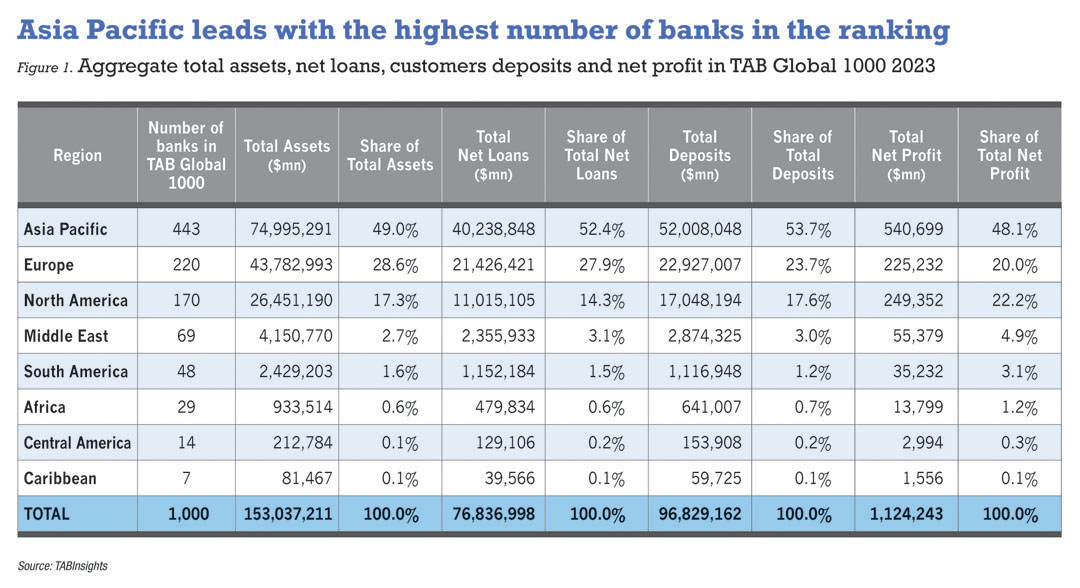

The world’s top 1000 largest banks collectively held $153 trillion in total assets, $76.8 trillion in net loans, $96.8 trillion in customer deposits, and generated a total net profit of $1,124 billion. This is according to TAB Global 1000 2023, an evaluation of the 1000 largest banks in the world for the financial year (FY) 2022, with a March 2023 cutoff.

This year marks a significant milestone as the ranking has been expanded to encompass 1000 of the largest banks in the world. The assessment spanned 98 countries and territories, including representation from 37 European nations, 22 countries and territories in Asia Pacific, 11 Middle Eastern countries, nine African nations, eight South American countries, four North American nations, four Caribbean nations, and three Central American countries.

Asia Pacific had the most banks in the ranking

The ranking of the world’s largest banks showcased a notable presence of banks from Asia Pacific, totalling 443 entities. Europe followed closely with 220 banks, while North America featured 170, the Middle East 69, South America 48, Africa 29, Central America 14, and the Caribbean region seven.

In terms of total assets, banks in Asia Pacific held the largest share at 49%, followed by Europe at 28.6%, North America at 17.3%, the Middle East at 2.7%, South America at 1.6%, and Africa at 0.6%. When it comes to net profit, Asia Pacific also led, with a share of 48.1%, while North America accounted for 22.2%, Europe for 20%, the Middle East for 4.9%, South America for 3.1%, and Africa for 1.2%.

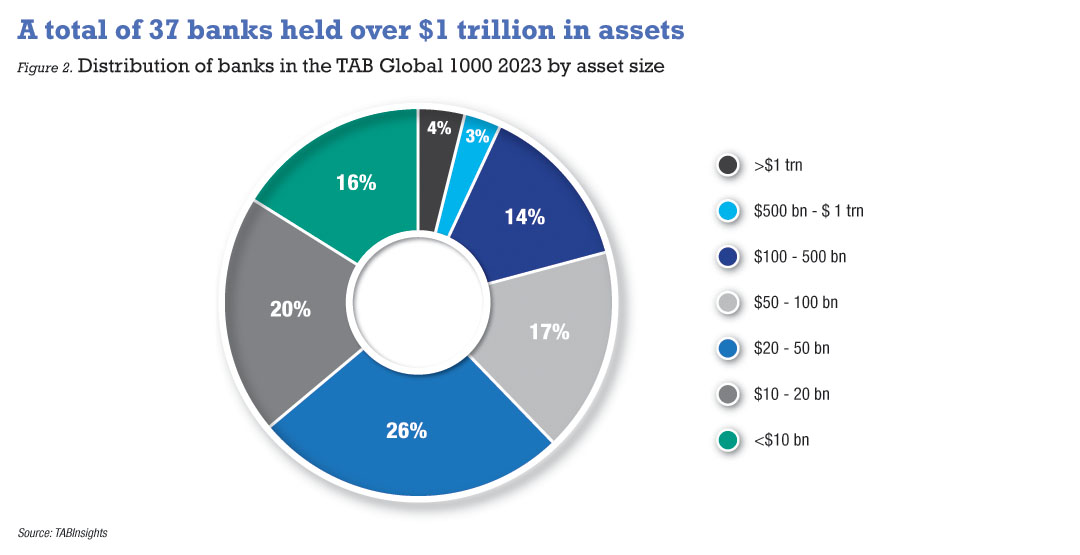

There were 37 banks with total assets exceeding $1 trillion, comprising 16 banks from Asia Pacific, 13 banks from Europe and eight banks from North America. Additionally, there were 169 banks with assets ranging from $100 billion to $1 trillion and 636 banks with assets between $10 billion and $100 billion.

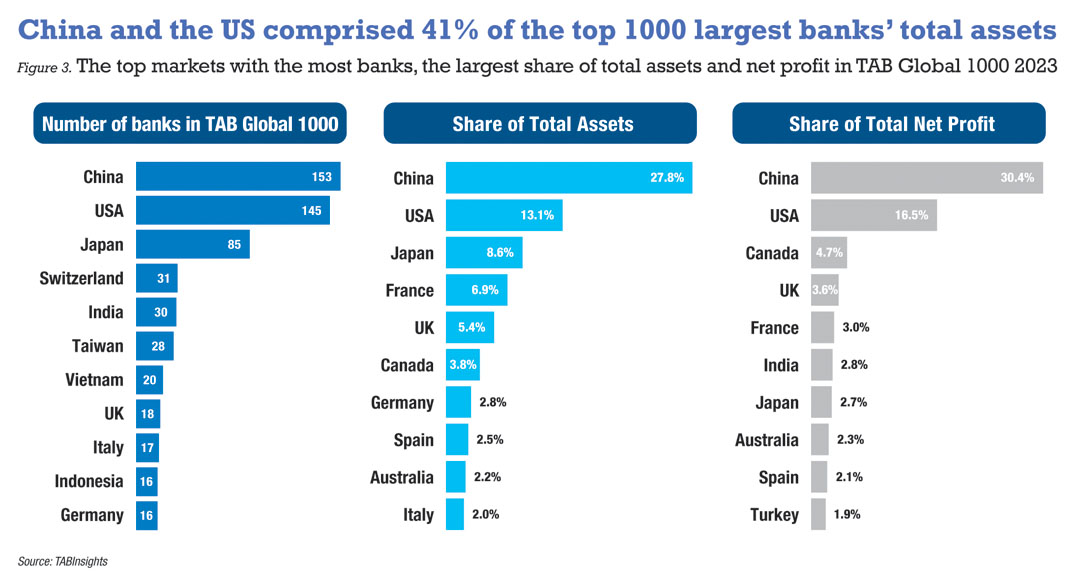

China and the US have the largest banking sectors

China led with the highest number of banks in the ranking, totalling 153, followed by the US with 145, Japan with 85, Switzerland with 31, and India with 30. Banks from China and the US also dominated in terms of total assets, comprising 27.8% and 13.1%, as well as in net profit share, accounting for 30.4% and 16.5%, respectively.

Despite having only seven banks represented, France contributed 6.9% of the aggregate total assets of the 1000 largest banks and 3% of the aggregate net profit. Similarly, Canada, with 11 banks, accounted for 3.8% of the aggregate total assets and 4.7% of the aggregate net profit. Spain, with eight banks, made up 2.5% of the aggregate total assets and contributed 2.1% to the aggregate net profit.

A total of 85 Japanese banks collectively generated only 2.7% of the aggregate net profit. In addition, the 31 Swiss banks represented just 1.4% of the combined total assets of the 1000 largest banks and contributed a mere 1.1% to the aggregate net profit.

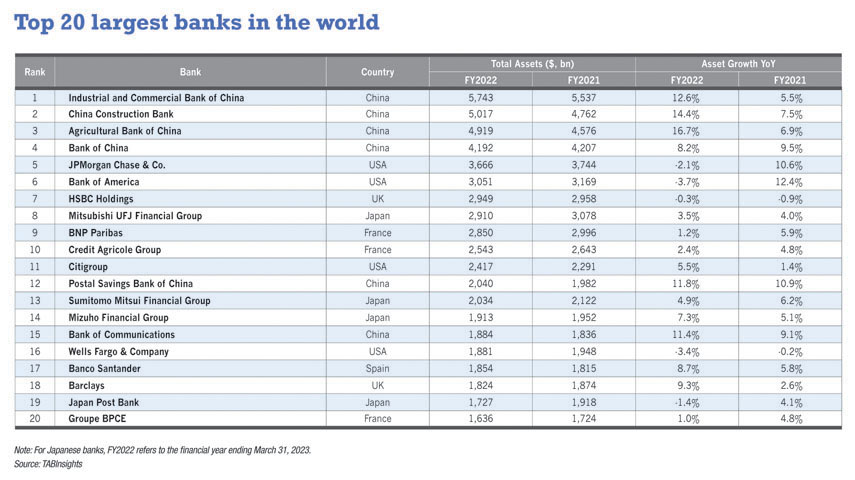

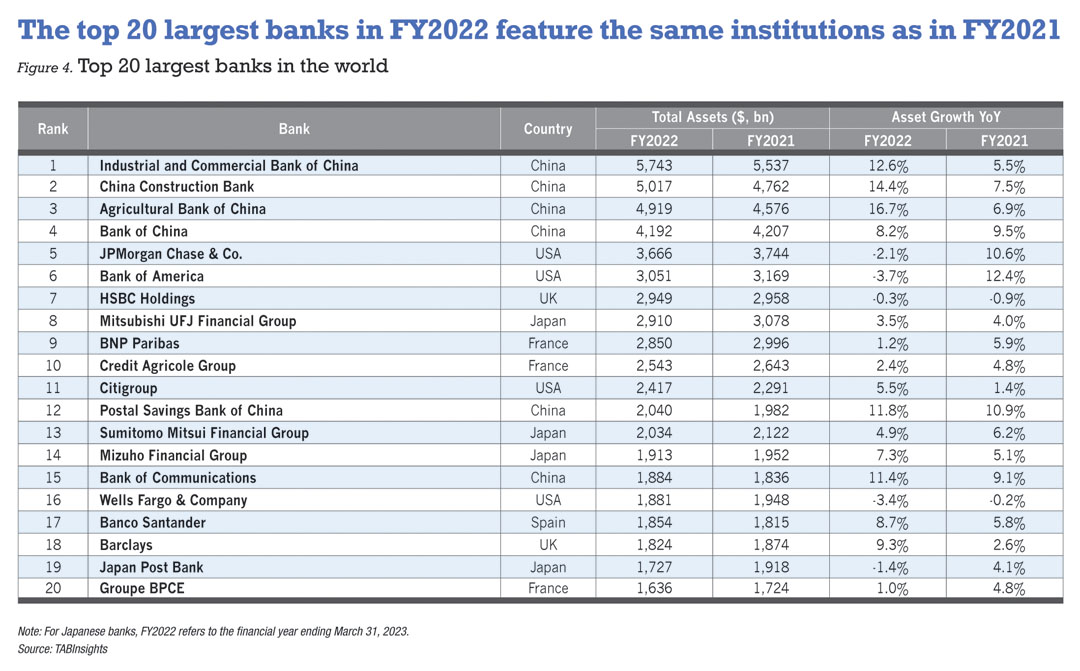

Top 20 largest banks in the world

The top 20 largest banks in the world remained unchanged at the end of FY2022 compared to FY2021, with only minor shifts within this top 20 group. The largest banks in China, France, Japan, Spain, the UK and the USA are among the top 20 largest banks in the world.

Industrial and Commercial Bank of China (ICBC) retained its title as the world’s largest bank, with China Construction Bank, Agricultural Bank of China, and Bank of China following closely. ICBC’s total assets expanded by 12.6%, reaching $5,743 billion by the end of FY2022. Notably, ICBC’s total assets surpassed those of JPMorgan, the fifth-largest bank globally, by 57%, up from a 48% lead in FY2021. Despite Renminbi depreciation, Chinese banks demonstrated stronger growth in FY2022.

All of the US banks within the top 20 largest banks in the world experienced a fall in total assets in FY2022, except for Citigroup. JPMorgan, Bank of America, and Wells Fargo saw declines in their total assets by 2.1%, 3.7%, and 3.4%, respectively. This can mainly be attributed to the reduction in deposits at financial institutions due to the US withdrawing monetary accommodation. Moreover, both Bank of America and Wells Fargo also recorded a decrease in their holdings of debt securities.

Total assets of Mitsubishi UFJ Financial, Sumitomo Mitsui Financial, and Mizuho Financial increased by 3.5%, 4.9%, and 7.3% in FY2022 ending 31 March 2023, respectively. Nevertheless, when measured in US dollars, their total assets contracted due to a significant depreciation of the Japanese Yen. Consequently, Mitsubishi dropped to the eighth position in the world’s largest banks ranking, while HSBC Holdings advanced to seventh place.

BNP Paribas slipped to ninth place due to subdued asset growth and the Euro’s depreciation against the US dollar. In FY2022, BNP Paribas and Credit Agricole recorded modest upticks in their total assets, with growth rates of 1.2% and 2.4%, respectively. Both banks saw an increase in loans while reducing their cash and central-bank balance holdings.

Asia Pacific

Chinese banks have consistently climbed the rankings among the top 20 largest banks in Asia Pacific, compared to Japanese banks, that have seen a decline in their positions. This shift can be attributed to the robust asset growth of Chinese banks. Postal Savings Bank of China surpassed Sumitomo Mitsui Financial to become the sixth largest bank in the region, while Japan Post Bank fell behind Bank of Communications in the ranking.

State Bank of India (SBI) surpassed ANZ to secure its position as the 20th largest bank in Asia Pacific. In FY2021, SBI’s total assets grew by 10.6%, followed by an 11.1% increase in FY2022. In contrast, ANZ saw a 6.1% decrease in total assets in FY2021, but rebounded with a 10.9% increase in FY2022.

There have been no changes to the rankings of the largest banks within each country or territory, except for Bangladesh and Pakistan. In Bangladesh, Islami Bank Bangladesh overtook Sonali Bank to become the largest bank, with its total assets growing by 12.3% in FY2022, compared to Sonali Bank’s modest 4.8% growth. Similarly, in Pakistan, National Bank of Pakistan surpassed Habib Bank to become the largest bank in the country. Land Bank of the Philippines is expected to surpass BDO Unibank to become the largest in the Philippines in 2024, owing to its merger with Development Bank of the Philippines.

Europe

Italy, the UK, Germany, and Switzerland had the highest representation among the top 100 largest banks in the world. The top largest banks in Europe includes HSBC, BNP Paribas, Credit Agricole, Banco Santander, Barclays, Groupe BPCE, Societe Generale, Deutsche Bank, Credit Mutuel and UBS.

Several countries witnessed changes in their largest banks. For instance, KBC Group overtook BNP Paribas Fortis as the largest bank in Belgium, Luminor Bank surpassed Swedbank Estonia in Estonia, Bank of Georgia replaced TBC Bank in Georgia, Eurobank took the lead over the National Bank of Greece in Greece, and Skandinaviska Enskilda Banken overtook Svenska Handelsbanken in Sweden.

North and South America

The top 10 largest banks in North America comprise six from the US and four from Canada. Among them, the Toronto-Dominion Bank, Canada’s largest, ranked sixth in North America and 25th in the world. The weighted-average asset growth of the four Canadian banks was 12.8% in FY2022, accelerating from 3.4% in FY2021. The six US banks saw total assets decline by 1.1% on average in FY2022, compared to an increase of 9.2% in FY2021. Mexico’s largest bank, BBVA Mexico, saw its total assets increase by 12.2% to $141 billion in FY2022, solidifying its position as the 24th largest bank in North America.

In South America, only three Brazilian banks, namely Itau Unibanco Holding, Banco do Brasil, and Banco Bradesco, secured spots among the top 100 largest banks globally. Among the top 10 largest banks in South America, five hail from Chile, four from Brazil, and one from Colombia. The largest banks in Peru, Uruguay, Ecuador, and Argentina ranked 12th, 18th, 19th, and 24th, respectively, in South America.

Middle East and Africa

In the Middle East, only Qatar National Bank and First Abu Dhabi Bank secured positions among the world’s top 100 largest banks. The top 10 largest banks in the Middle East comprise three UAE banks, two Saudi Arabian banks, two Israeli banks, and one each from Egypt and Qatar. This year, Egypt falls under the Middle East category instead of Africa. Among the top 10, National Bank of Egypt and Al Rajhi Bank posted the most substantial asset growth at 35.2% and 22.1%, respectively, in FY2022.

None of the African banks featured among the world’s top 100 largest banks. Standard Bank Group, with total assets of $170 billion at the end of 2022, has maintained its position as the largest bank in the region, ranking 143rd in the world. Following closely are FirstRand, Absa Group, and Nedbank Group. The largest banks in Morocco, Nigeria, and Togo ranked fifth, ninth, and 10th in Africa, respectively. Meanwhile, KCB Group has surpassed Equity Group to become Kenya’s largest bank, securing the 16th position in the region.

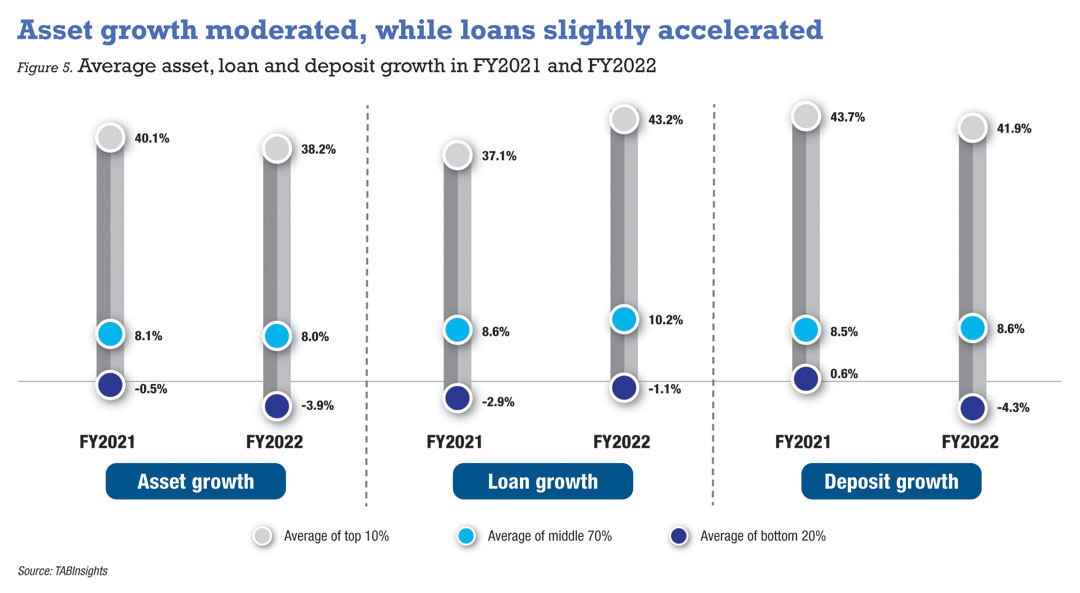

Asset growth decelerated

The weighted asset growth of the top 1000 banks experienced a moderation, reaching 6.4% in FY2022, down from the 7.4% recorded by the same group of banks in FY2021. This slight decline in asset growth can largely be attributed to the deceleration in North America and Europe, whereas banks in Asia Pacific and Africa reported stronger asset growth in FY2022 compared to the previous year.

Customer deposit growth among these 1000 banks also decelerated, shifting from 8.7% in FY2021 to 6.9% in FY2022. However, there was an improvement in net loan growth, that rose from 7.7% in FY2021 to 8.7% in FY2022. Despite a slowdown in deposit growth, North American and European banks experienced accelerated net loan growth in FY2022.

In North America, Canadian and Mexican banks exhibited robust balance sheet growth in FY2022. Conversely, US banks experienced a substantial slowdown in asset growth, decreasing from 9.7% in FY2021 to 1.8% in FY2022. While loan growth remained stable at 9.2%, banks here witnessed reductions in deposits held at financial institutions and debt securities holdings. Moreover, customer deposits declined by 0.1% in FY2022, as depositors pursued higher-yielding alternatives due to the Federal Reserve’s aggressive interest rate hikes.

In Europe, average asset growth decelerated from 5.1% in FY2021 to 2.5% in FY2022, marking the weakest performance among all regions. On average, Italian, Portuguese, and Dutch banks witnessed declines in assets by 5.2%, 1.6%, and 0.6%, respectively. Additionally, asset growth in countries like Switzerland, Denmark, the UK, France, and Belgium remained below 2%. On average, loans and deposits at Swiss banks contracted by 0.6% and 1.3%, respectively, despite a marginal 0.2% increase in assets. Meanwhile, the UK experienced the most substantial decline in bank deposits among European countries, with a 0.6% decrease. Turkey, within the European market, stood out with the highest asset growth, as Turkish banks achieved a remarkable average asset growth surge of 58.9% in a high-inflation environment.

The average asset growth of banks in the Asia Pacific region showed a slight improvement, rising from 7.8% in FY2021 to 8.9% in FY2022. Countries such as China, Malaysia, the Philippines, and India experienced accelerated asset growth. Pakistan, Vietnam, the Philippines, India, and China recorded double-digit increases in their assets. Despite some decline, Pakistan’s banks maintained the highest asset growth in the region. Chinese banks, while seeing asset growth accelerate from 8.3% in FY2021 to 11.5% in FY2022, observed a slight dip in their average loan growth from 12% to 11.7%.

Conversely, the asset growth of banks declined in several markets, including Bangladesh, Japan, Thailand, and Hong Kong. Among them, Japan, Hong Kong, and Thailand registered the weakest asset growth in the region, at 1.9%, 2.9%, and 3%, respectively. Hong Kong banks, on average, saw a 2% drop in loans, primarily due to subdued loan demand attributed to elevated borrowing costs and economic uncertainty.

African banks stood out with the strongest balance sheet growth compared to all other regions, except for the Middle East, where several mergers and acquisitions occurred over the past two years. Nigeria is among the countries with the most robust asset growth in the world. Nigerian banks saw asset growth accelerate from 18.2% in FY2021 to 23.4% in FY2022. South African banks also observed an uptick in asset growth, reaching 6.6%, although it remained relatively low. Despite this, South African banks recorded a decline in deposits, while loan growth accelerated.

What is TAB Global 1000?

TAB Global 1000 is an annual study of the financial and business performance of the global banking industry. The study comprises two different lists: the first ranks the top 1000 banks in the world by asset size, while the second ranks the same 1000 banks by strength, an evaluation that is predicated on the belief that a strong bank demonstrates long-term profitability from its core businesses.

Which banks are included?

The rankings encompass all major regions in the world, including Africa, Asia-Pacific, the Caribbean, Central America, Europe, the Middle East, North America and South America. The assessment covers both banks and financial holding companies with significant activity in banking. It excludes central banks, policy banks and finance companies.

How do we collect and treat the data?

Bank annual reports are our main sources of data. In the absence of up-to-date annual reports, we contact banks directly to source financial results. Consolidated figures are used for banking groups, except when non-banking activities form a substantial portion of the consolidated figures, in which case we look at the banking unit independent of its parent. All figures are quoted in US dollars. Year-on-year growth rates are calculated based on original local currency figures.

.png)

.webp)