Research Notes Nov 07

Premium

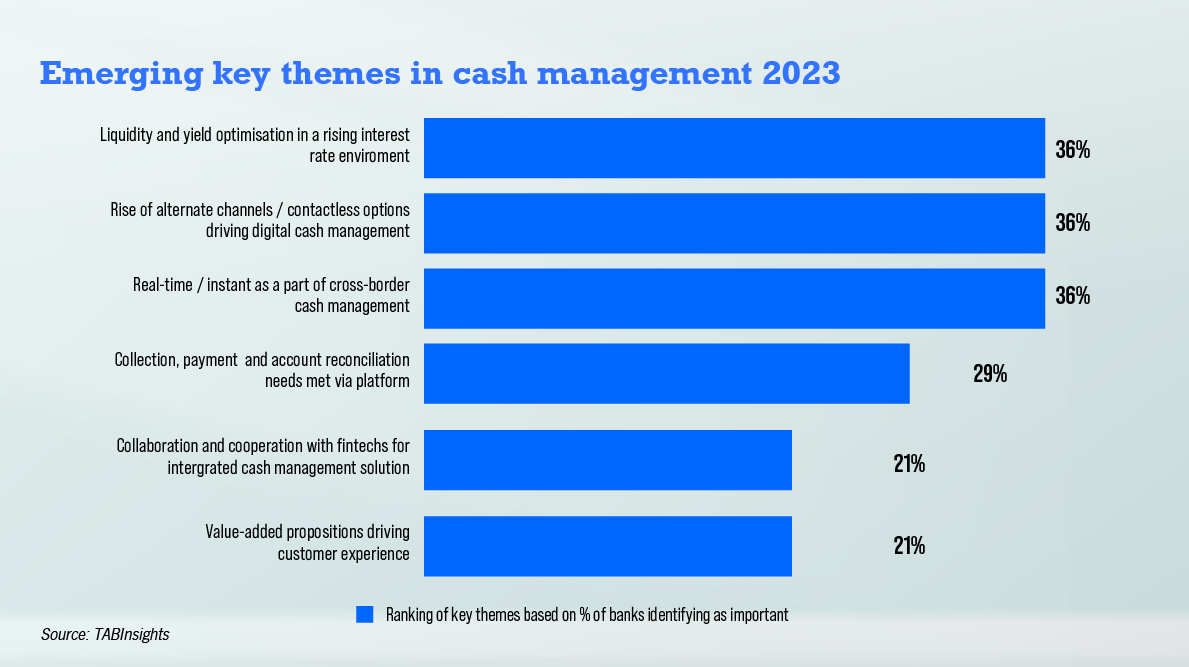

An altered operating environment has led treasury to reprioritise their investment and liquidity management strategy, with cash management providers offering enhanced solutions