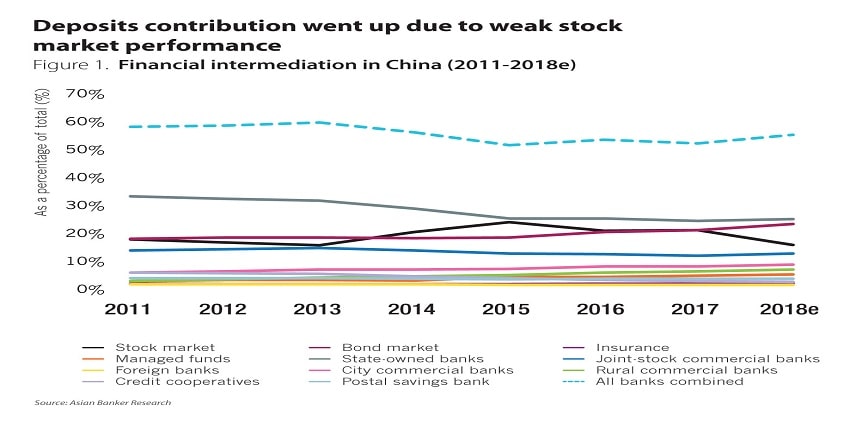

This year’s Asian financial intermediation trend report has shown a slight displacement of stock markets in favour of bond markets, banking institutions and managed funds as destinations for investible fund flows, on the back of mounting nervousness over the impact of the ongoing US-China trade tension and rising interest rates on economic growth in the region.

Stock markets

All the nine Asian economies covered in the report experienced a decline in their stock market contribution to total investible fund in 2018, and their stock market capitalisation also shrank significantly. In these markets, about $3.8 trillion in market capitalisation was wiped out in 2018. The escalating US-China trade war led to concerns over economic downturn and pulled down Asia’s major stock indexes, and the stock markets were also significantly affected by rising US interest rates. The MSCI AC Asia ex Japan Index slumped 16.4%, the worst since 2011. The benchmark Shanghai Composite Index was the worst performing equity market in the region in 2018, and the index tumbled 24.6%, its sharpest drop since 2008. South Korea’s KOSPI Index plunged 17.3%, and Hong Kong’s Hang Seng Index lost 14.8%.

Among these markets, Hong Kong saw the most significant decrease in its stock market contribution to total investible fund in 2018, while the stock market capitalisation in China and South Korea registered the largest fall. The share of stock markets in total investible funds in Hong Kong declined from 54% in 2017 to 48%, and stock market capitalisation fell by 12% to $3.8 trillion. In China, the combined market capitalisation of Shanghai Stock Exchange and Shenzhen Stock Exchange dropped by 23% to $6.3 trillion. This was largely triggered by China›s slowing economy, the trade war with the US, the depreciation of renminbi and worries over Chinese corporate earnings.

Bond markets

Bond market contribution to total investible funds in all the nine economies went up in 2018. The aggregate amount of outstanding bonds in these markets reached $14.26 trillion as at the end of 2018, which grew at a compound annual growth rate (CAGR) of 12.2% between 2011 and 2018, higher than the CAGR of their aggregate stock market capitalisation during the same period, at 7.7%.

Among these economies, China and Indonesia witnessed the fastest growth in bond markets. The amount of outstanding bonds in China increased by 14% and the share in total investible funds went up from 20.5% in 2017 to 22.6%. In China, the issuance of local government bonds was accelerated to fund infrastructure development, in order to offset the effects of the trade war with the US and stimulate the economy. In addition, the growth was also driven by the increase in the amount of outstanding commercial bank bonds, as banks raised capital to strengthen balance sheets. Indonesia’s bond market is dominated by government bonds, which expanded by 15%, as treasury bills and bonds were issued by the Ministry of Finance for budget financing.

In most economies, stock market contributed more to total investible funds than bond market, but China and South Korea were the exceptions. South Korea had the largest share of bond market in total investible funds, while the share of bond market in total investible funds in Hong Kong was the least, at 3.1%. South Korea and Hong Kong registered the lowest growth rate in bond market at 3.6% and 2.3%, respectively.

Banking institutions

In 2018, the deposits of banking institutions contributed 56.4% to total investible funds in China and more than 35% to total investible funds in markets like Indonesia and the Philippines, while the deposits contribution was less than 25% in markets such as Hong Kong and Singapore. Overall, bank deposits regained some ground amid the turbulence in regional stock markets in 2018. China and the Philippines saw the biggest increase in deposits contribution to total investible funds by 2.8% and 2.4%, respectively.

Managed funds and Insurance

Managed funds saw strong growth in the region due to growing demand. The share of managed funds in total investible funds in the region showed an upward trend. However, it should be noted that the figures for managed funds are not computed on a similar basis among countries. Among these economies, Hong Kong and Singapore had the largest shares of managed funds in total investible funds.

The level of insurance contribution to total investible funds remained extremely low. Among these economies, South Korea possessed the highest share of insurance in total investible funds, at 2.5%. However, the premium income of life insurance firms in South Korea decreased for two years in a row, due to market saturation and weaker demand. China, Hong Kong and India continued to post high growth of over 10%.

Asian stocks witnessed some recovery in the beginning of 2019. Stock markets continue to face significant downside risks, largely due to slowing economic growth and upcoming elections in some Asian countries. However, the US-China trade war is expected to head towards a certain future resolution, and the US Federal Reserve will slow the pace of interest rate hikes. Meanwhile, the turbulence in Asian stock markets last year has made Asian stocks cheaper in terms of price valuations. More investible funds are expected to flow into stock markets in 2019.

Note: To illustrate the role of financial intermediation (from the funding perspective) of different institutions—including banking institutions, stock markets, bond markets, insurance companies and managed funds—data on annual deposits, stock market capitalisation, amount of outstanding bonds, premium revenues and assets under management were used to calculate the corresponding market shares of total investible funds of the markets covered. Though we have made every effort to make the data comparable and complete, we acknowledge that there may be some discrepancies due to differences in classification and categorisation of intermediaries. This report provides an update on financial intermediation data over the period 2011–2018.

.png)

.webp)