Datafiles

Jan 27

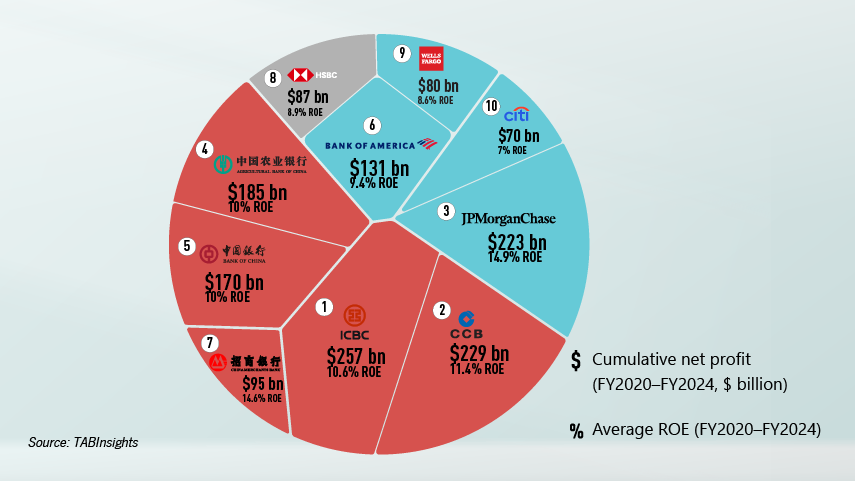

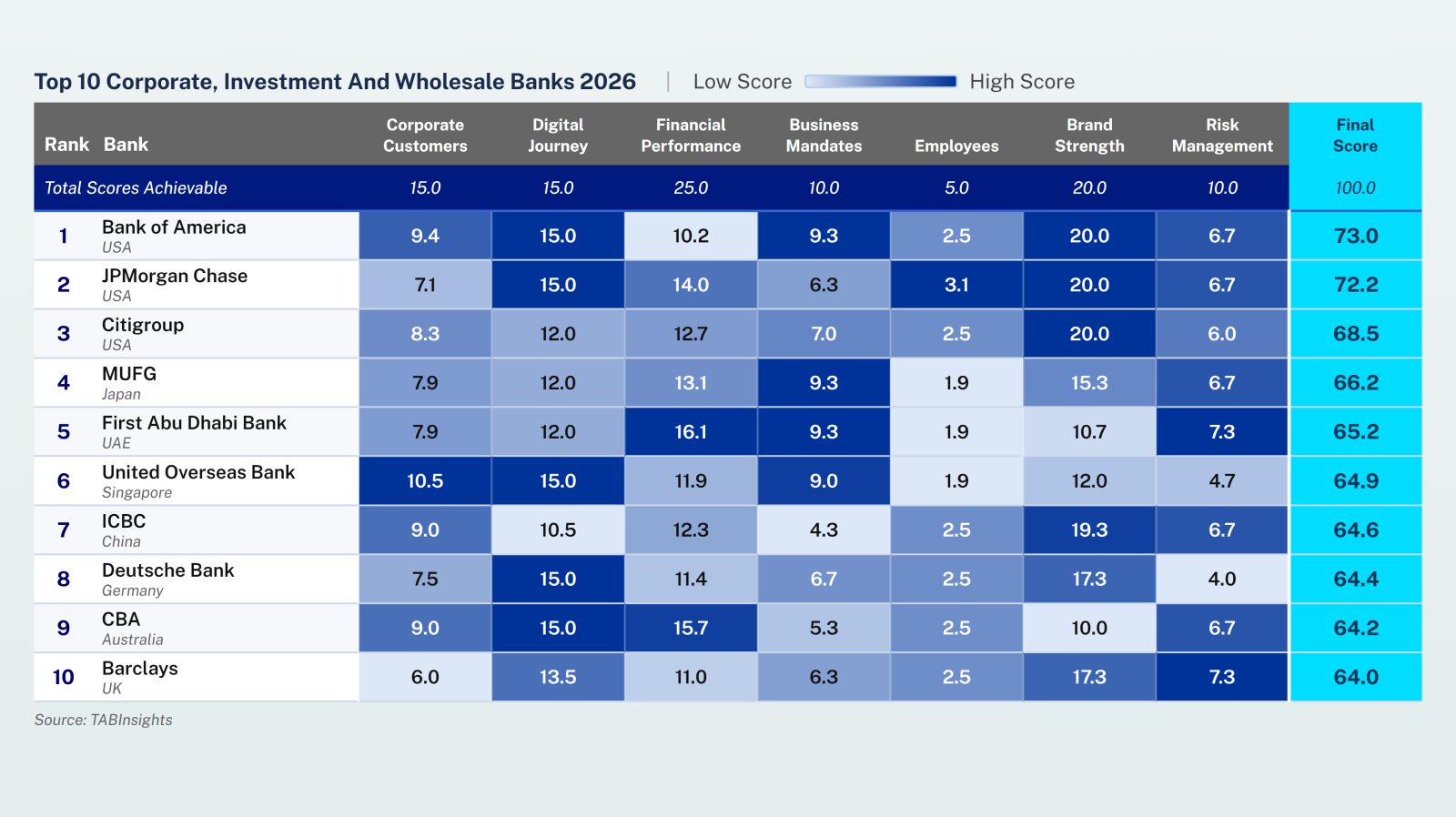

Chinese and US megabanks generate the largest absolute profits through scale and diversification, while emerging-market banks deliver higher — but more volatile — returns on equity.

.png)